Fact or Fiction?

2023 has been mixed in terms of economic data but markets in the balance have been moving upward. Both stocks and bonds have seen upward movement over the past three and a half months:

While markets have been moving in the right direction, there has been no shortage of unsettling news. We’ve heard talk of recession fears, geopolitical turmoil, and issues with the banking sector. The combination of these factors along with the antecedent anxiety from last year’s decline have reinforced investor skepticism. In times of pessimism, investors can become easier marks for those who peddle investment theories that may not be grounded in sound fundamentals. For this quarter’s Insights, I thought it might be useful to review some commonly circulated ideas that may or may not be accurate.

Idea #1: The best days for bonds are in the past and after last year’s bond turmoil, bonds should no longer be a part of my portfolio.

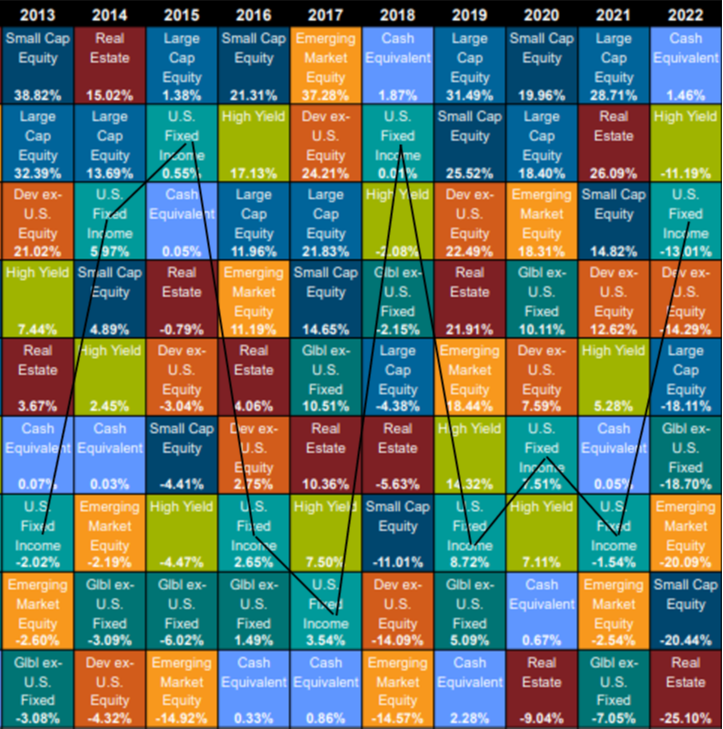

In our view, this idea is fiction. Asset classes that have been beaten down are easy targets, but investors will often forget the cyclical nature of markets. When one investment “zigs” the following year it often “zags”. Consequently, those who chase performance tend to buy and sell at the worst possible times. Consider market leadership over the past 10 years and note how fixed income (bonds) has migrated up and down the leaderboard over time:

Source: Callen Institute, markup added

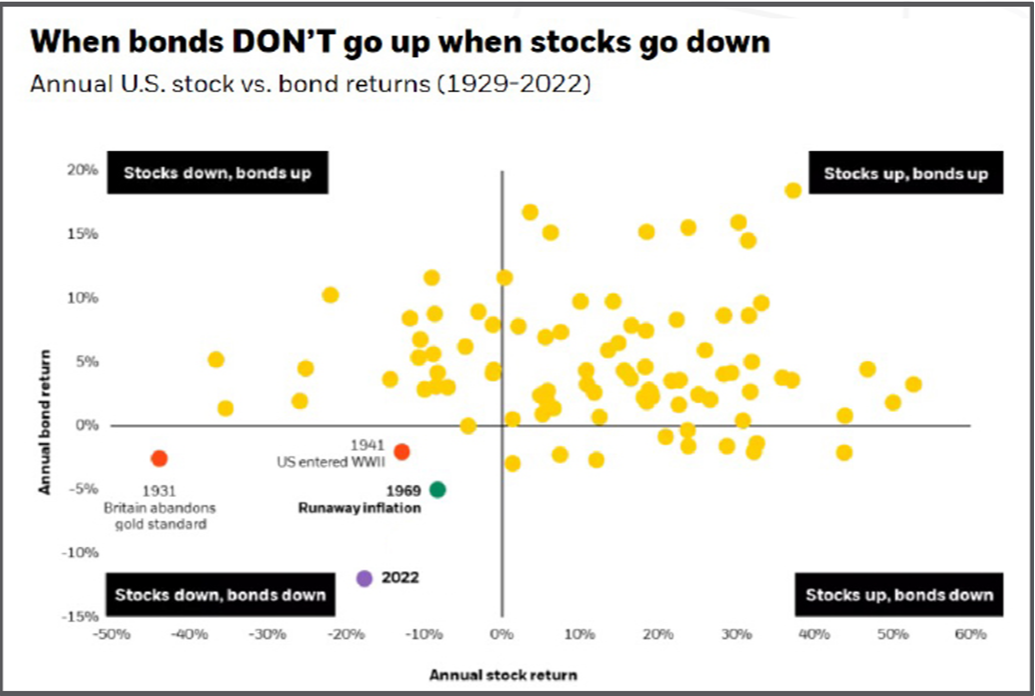

Also observe how infrequent years like 2022 are where both and stocks and bonds were down. There have only been four years since 1929 where both stocks and bonds have declined in the same year:

Source: Brinker Capital

Bonds remain an important part of a diversified portfolio and far more often than not help hedge in down markets.

Idea #2: A recession is imminent and markets will crater with this happens

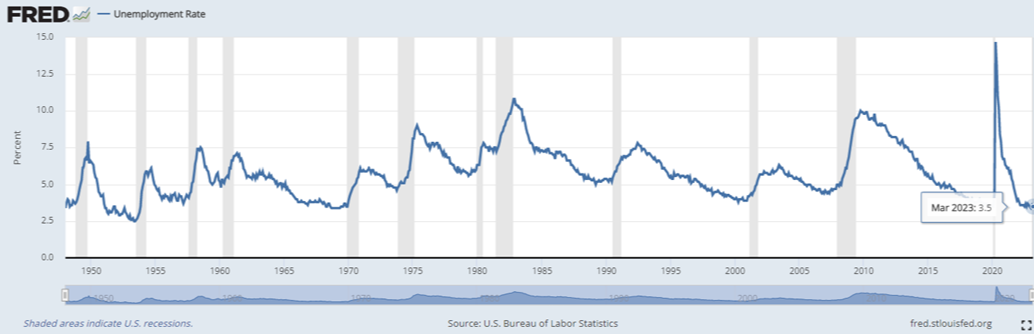

While this isn’t clear fact or fiction, neither a recession nor a subsequent market decline is a given. On the recession front, we are seeing a slowing economy, but labor remains strong. While recession is possible, said recession would likely be of the more mild variety. Whether or not a recession happens will be a function of how the complicated stew of employment, inflation, and interest rates evolves over next several months. On the employment front, unemployment rates remain near historical lows:

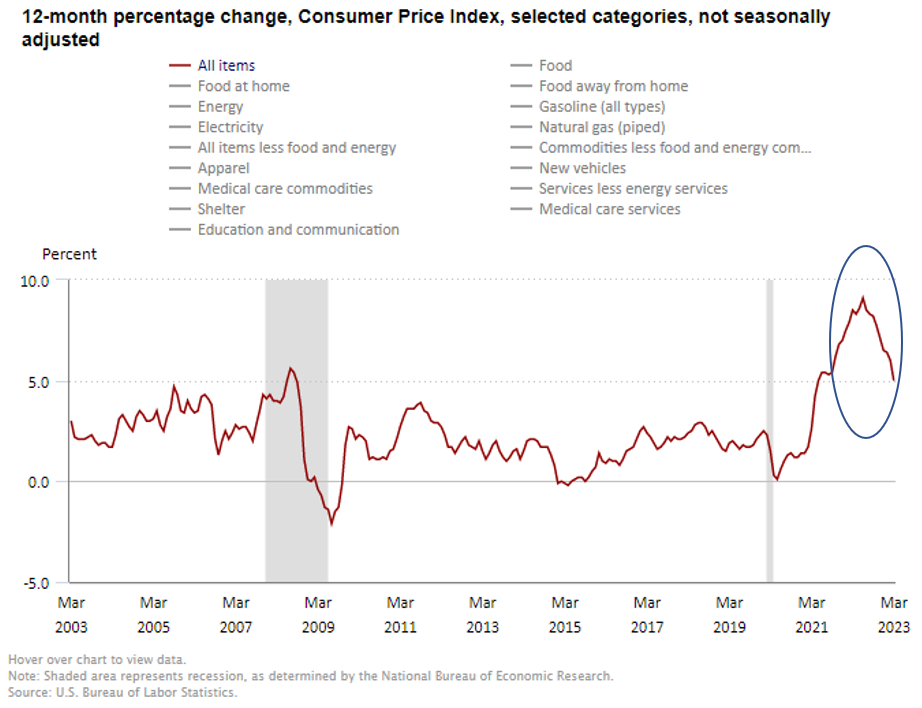

Strong labor markets are inconsistent with recession and we’ve yet to see a strong labor pullback. On the inflation front, we have seen inflation receding, but it still remains stubbornly high:

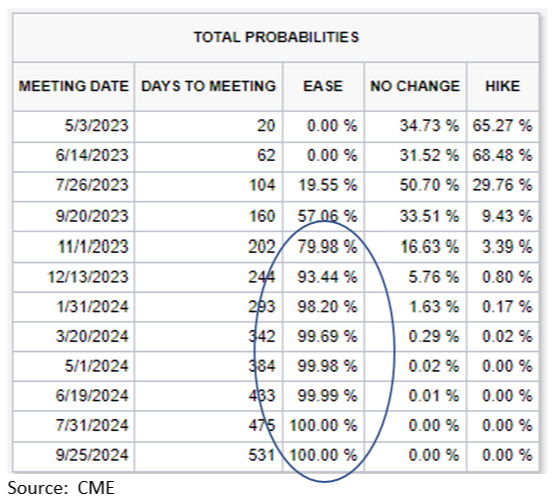

With respect to interest rates, futures pricing suggests a strong likelihood of rate decreases for the back half of the year and into 2024:

Earnings have shown signs of softening and credit growth has slowed (both indicators of a slowdown), but the strong employment market muddies the picture. Our view is that a recession is not a lock. Moreover, it’s important to keep in mind that recessions lag the market. This means that the market typically bottoms out prior to the economy bottoming out and markets usually start to recover before the actual economy.

Idea #3: The US dollar is rapidly losing its status as the world’s reserve currency

Mark Twain is rumored to have said that the “reports of my death are greatly exaggerated”. So it is with the US dollar, and we view the notion that the demise of the US dollar is imminent as fiction. Consider what the US dollar has done relative to a basket of other currencies over the past 12 months:

Source: Wall Street Journal

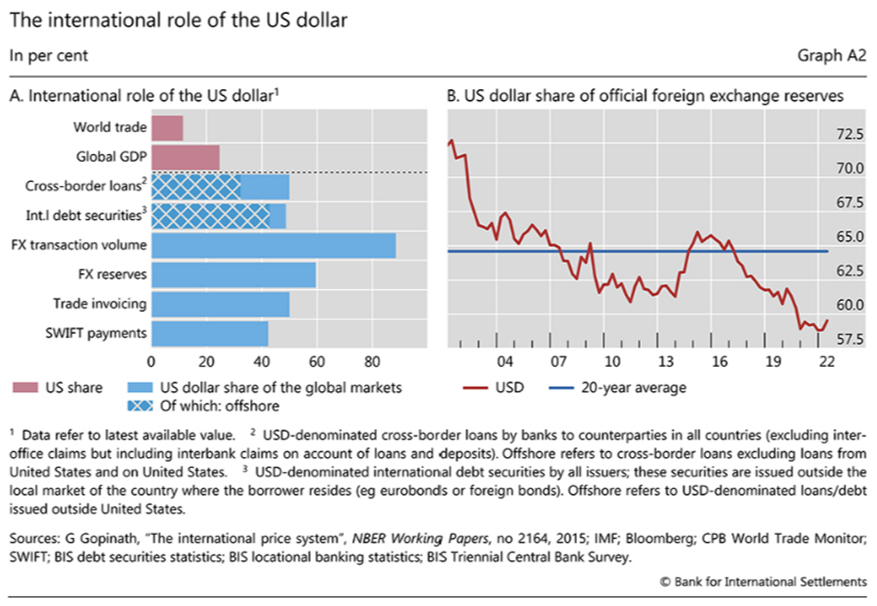

Against a backdrop of high inflation and ballooning public debt, the US dollar appreciated in value. There are several reasons for this, but perhaps most central is the idea that the US dollar is the least bad option. A reserve currency is a place where economic actors can place funds and have high confidence in the long-term stability of those funds. In spite of the challenges that the US faces financially, it remains on firmer footing than potential replacements. Other currencies are either backed by disjointed and incomplete economic and political union (the Euro), have their own significant fiscal issues (i.e. the Yen; Japan has a debt to GDP ratio of >200%), are too small (the Swiss Franc), or the sponsoring country has a checkered record of adherence to rule of law (the Yuan). For the foreseeable future when there is a flight to safety (wars, economic upheaval, etc.), the US dollar remains the prohibitive favorite. While other currencies are making some inroads as alternative vehicles for global commerce, the dollar remains dominant:

Idea #4: With the turmoil we’re seeing in the banks, this is 2008 all over again

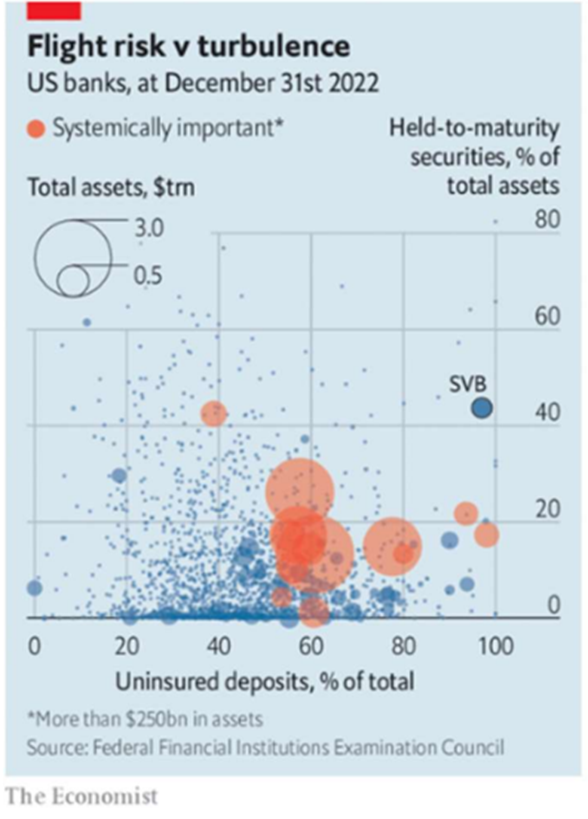

2008 was an incredibly turbulent year and represented the greatest amount of financial turmoil since the Great Depression. As 2008’s troubles were centered around financial institutions, some have wondered if the recent turmoil with the banks will cause a repeat of 2008. In our view this assessment is more fiction than fact. If we compare key drivers of the 2008 crisis, the financial system of 2023 appears to be in far better shape:

Bank concerns have cooled significantly over the past few weeks and the trigger of the bank concerns (Silicon Valley Bank’s failure) was a somewhat unique situation. Silicon Valley Bank had the following going against it:

- Over 90% of its deposits were over the $250k FDIC insurance max per account

- It had over 40% of its assets in “held to maturity” securities (which were largely underwater due to rate increase)

- Significant exposure to one industry (technology)

- Lacking a “systemically important” designation

As it became apparent that 1.) the government was going to step and prevent contagion by backstopping all of Silicon Valley Banks deposits and 2.) Most banks did not have similar issues, much of the concern started to abate.

We’ve enjoyed meeting with many of you over the past several months and look forward to those meetings coming up. As we enter the warmer months, we wish all of you the very best.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Diversification, asset allocation and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Investing involves risk, including loss of principal. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve. Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Alliance Wealth Advisors, LLC, is registered as an investment advisor with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability a SEC Registered Investment Advisor – 1148 West Legacy Crossing Blvd., Suite 110, Centerville, UT 84014.